Blockchain and Web3 Explainer

This is my blockchain and web3 explainer. There are many like it, but this one is mine.

Unfortunately, this piece is kind of like eating your vegetables - its not super enjoyable but its necessary to understanding the exciting applications of blockchain.

It’s also not going to answer every question you have. For some questions, this article should serve as a jumping off point into other research or even other pieces I’ve written. For others, there are no answers - people are working to solve those problems right now; its one of the reasons this space is so exciting!

Similar to the new concepts and terminology we had to learn in the early days of the internet, understanding blockchains requires a mind open to new ways of solving problems. There are countless articles in the late-90s, early 2000s declaring the internet dead following the the bursting of the dot-com bubble. Barron’s “Amazon.bomb” article is one of the most infamous.

After a few topline points, we’ll cover the basics of blockchain, the basics of web3, and an abbreviate history of blockchain technology.

Topline:

Quick hits on blockchain

Definition

Blockchains are a digital ledger that allow parties to transact without the use of a central authority as a trusted intermediary.

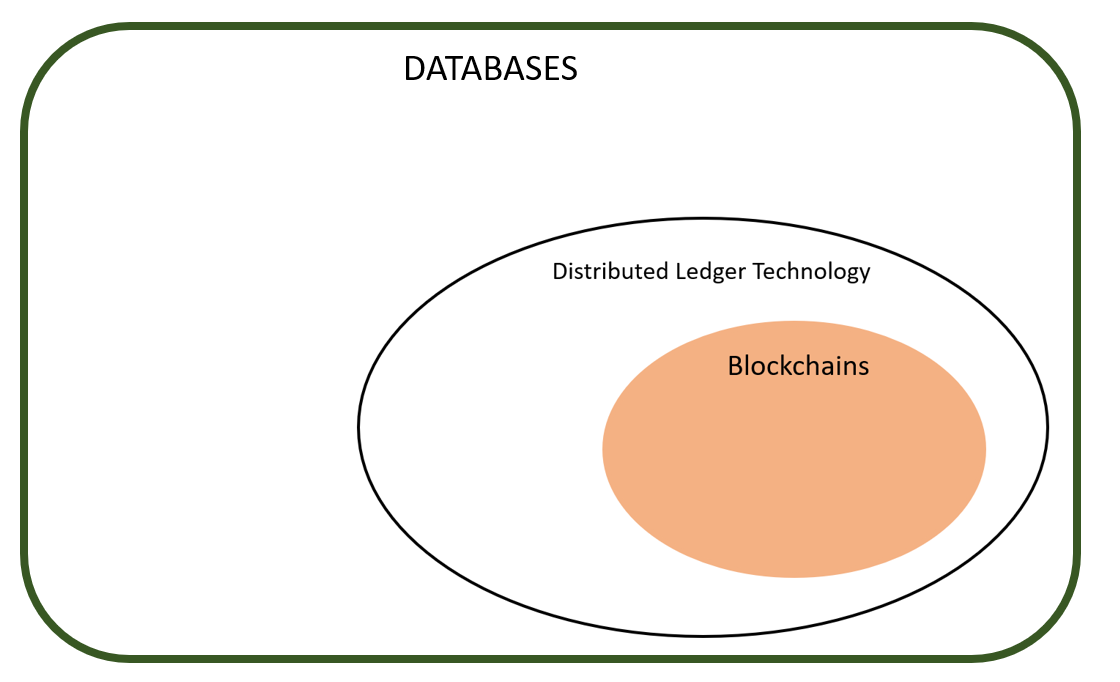

What type of technology is it?

Blockchains are a subset of Distributed Ledger Technology (DLT), which is itself a subset of Databases.

Databases are organized collections of structured information, or data, typically stored electronically in a computer system.

Distributed Ledger Technology is a digital system for recording interactions with a database in a manner where there is no central data storage or administrator.

Blockchains are a specific DLT architecture which we will explore in more depth below. Blockchains are the dominant DLT use case.

Why should I care?

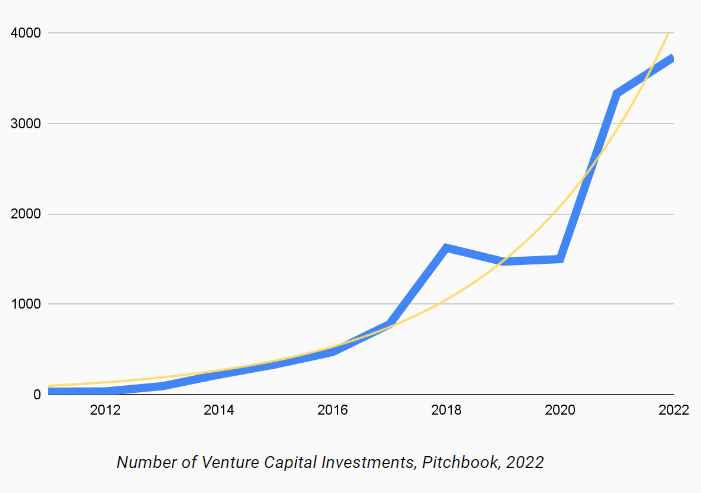

As of 2022, venture capitalists have invested more than $188.7 Billion in blockchain related startups. Today, there are more than 12,500 blockchain startups globally.

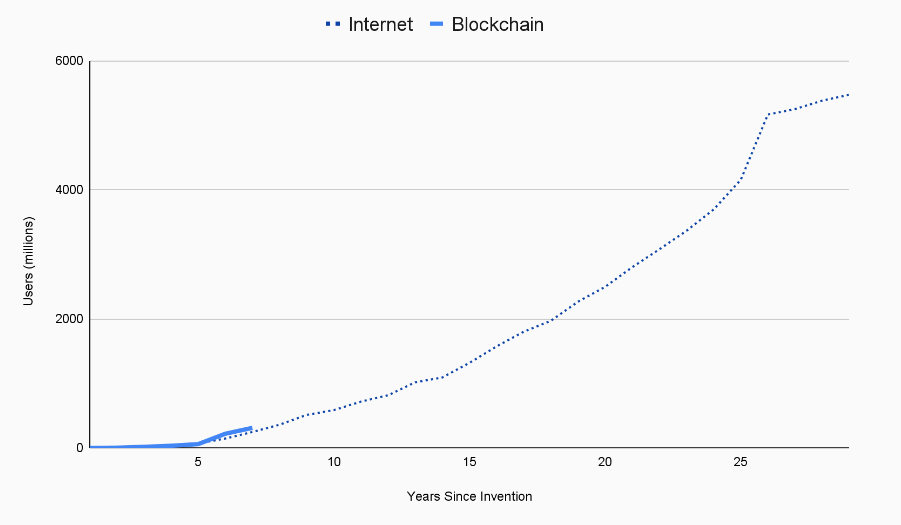

According to one Wells Fargo investment report, from invention to adoption, blockchain is growing at a similar pace to the internet in the 1990s. According to a 2021 Morning Consult poll, 1 in 6 U.S. households own a token secured by a blockchain.

Further, the world’s largest brands are exploring how they can integrate blockchain into their business. Starbucks integrated non-fungible tokens (NFTs) into its loyalty program. Nike launched an NFT platform, Swoosh, for digital sneakers. Reddit minted 10.6 million collectible avatar NFTs.

For most people - you may not need to care about blockchains specifics. Today, do you really care if Twitter uses a MongoDB or MySQL database? Unless you are a power user, probably not. In the same way that you dont need to know how to code to use and enjoy Twitter, you dont need to know all the ins and outs of blockchain to use and enjoy the applications built on top of it.

Blockchains:

The Trust Layer

I often find the easiest way to explain something as dense and technical as blockchain is to draw it out to help ensure the reader doesn’t get bogged down in technical jargon or miss a crucial sentence.

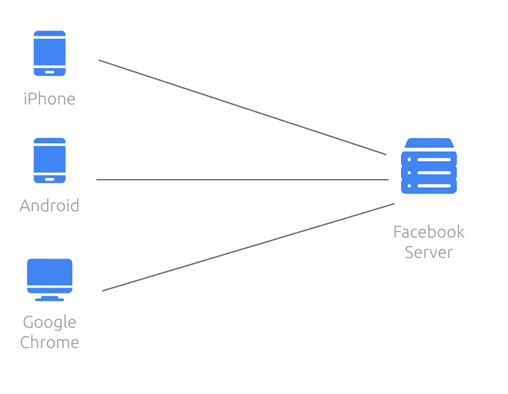

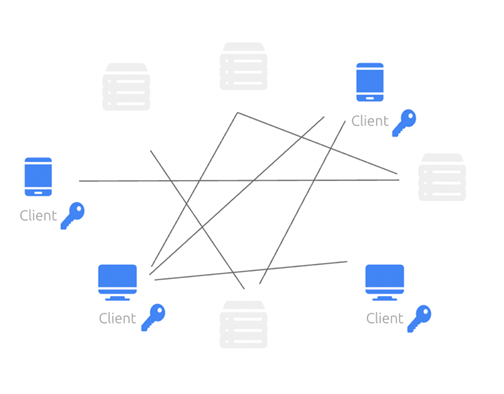

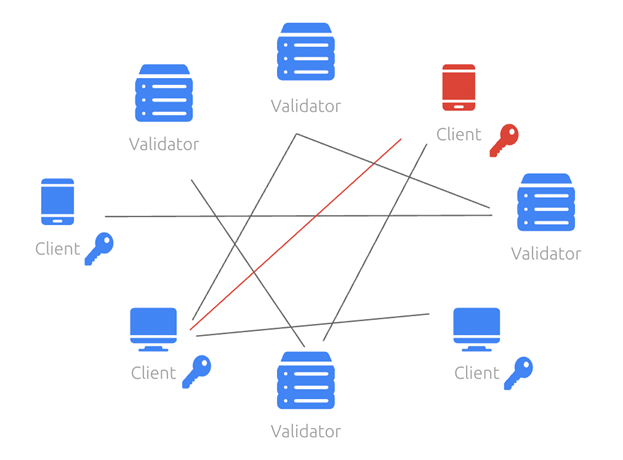

A traditional internet connection, the client-server model, is based on centralized servers which outside users may connect with to be served content.

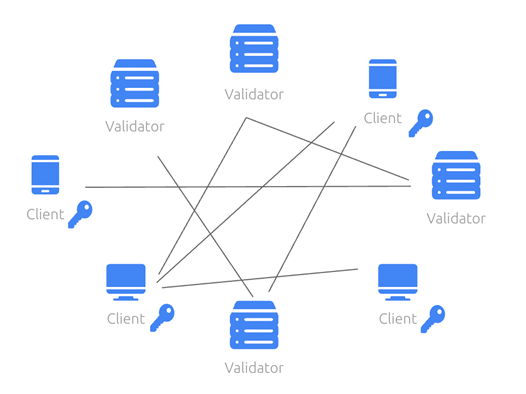

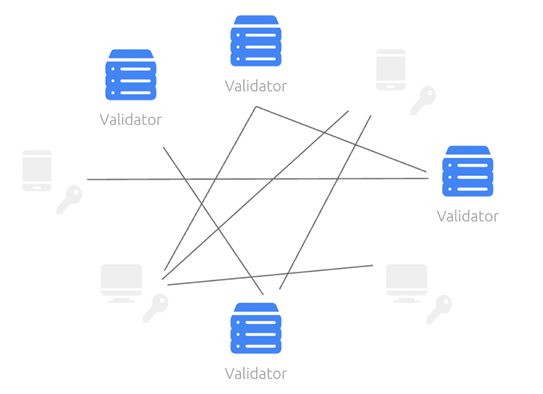

In contrast, blockchains are peer to peer networks.

Validators, often called miners, are incentivized to keep the network honest.

Clients (users) can send, receive and read interactions with the blockchain.

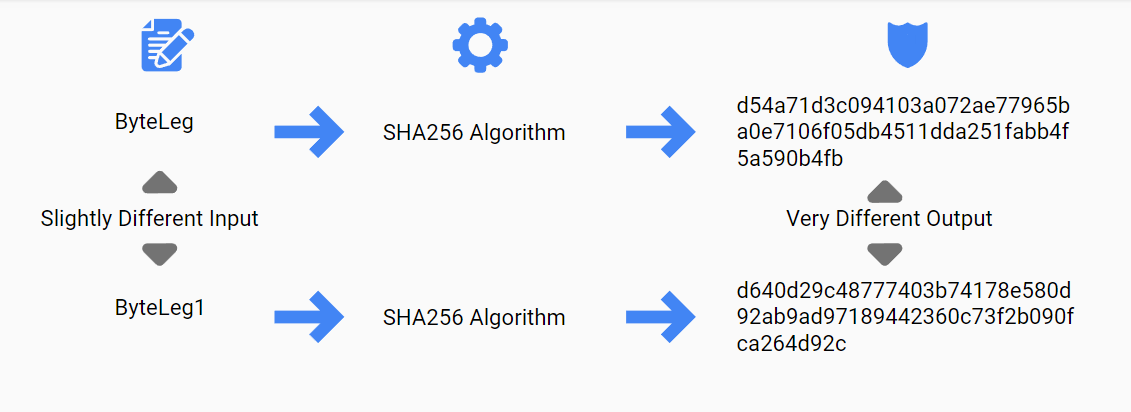

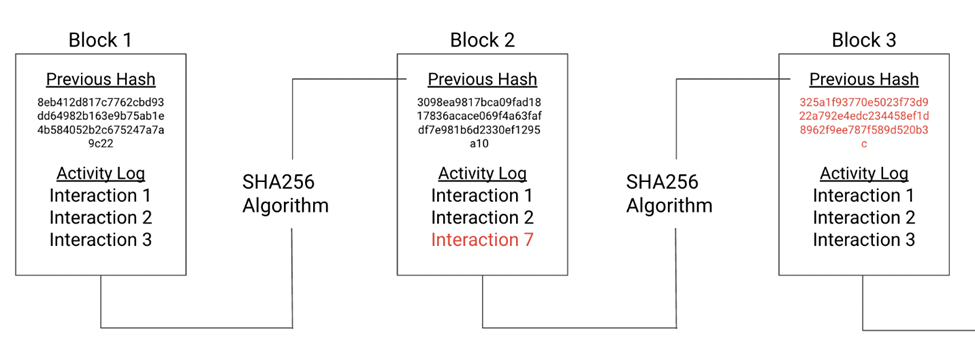

Hashing is a cryptographic technique to input text on one end and received encrypted text on the other end. The output is unique but is always the same length, no matter the size of the input text. Slight changes to the input lead to drastic changes in the output. The above is an example of how a hashing function might work.

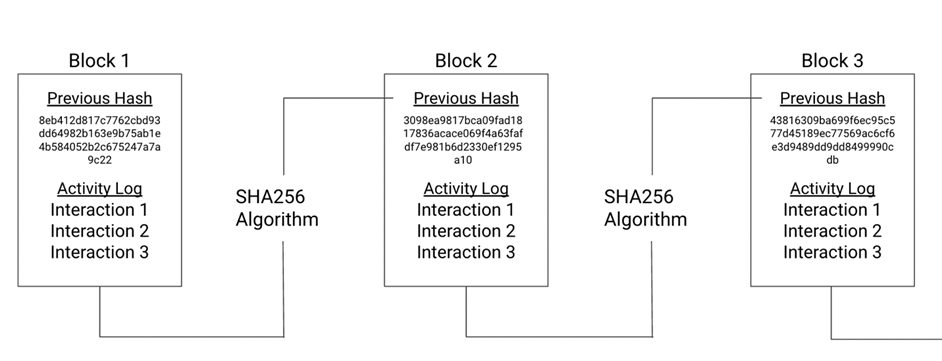

For blockchains, groups of transactions are grouped (blocks) and then used as an input into a hashing function (hashed). By putting the hash of each block at the top of the next grouping of transactions, blocks can be chained together cryptographically.

Because the hash values are inserted into the head of each block, any alteration to a previous block would alter output hash (seen above).

Because blockchains are a continual stream of blocks, any change to the history of a blockchain would cascade down the chain, alerting everyone of the bad actor.

For this reason, even if users don’t trust each other, they can trust the cryptography of the blockchain. This new, trustable network enables new businesses and use cases.

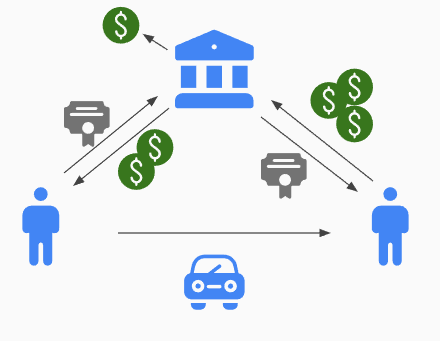

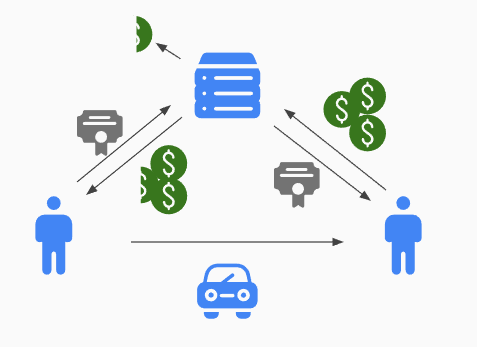

Today, large parts of our lives are mediated by someone because some people are not trustworthy. If you go to buy a car, an IOU written on a loose piece of paper isnt enough. Instead, they require you to use a bank to intermediate the trade, because they dont trust. If you dont make your car payments, the bank is listed as the lien holder and can seize your car. At its most basic level, because the bank is taking on the risk that you can’t be trusted, the bank receives a small fee.

The problem is that this still required everyone to trust someone: the bank. Blockchain fixes this. Instead of relying on a bank to mediate the transaction, code running on a trusted blockchain could. This is the original insight of Bitcoin.

However, its not just our financial transactions which are mediated by trusted third parties. Amazon and Ebay matches buyers and sellers online. Social media companies pick which content you see. Apple’s App Store picks which apps are available for download. In nearly all cases, when online, you are not directly interacting with someone but are instead interacting with them through a service.

Web3:

The Internet Built on Blockchains

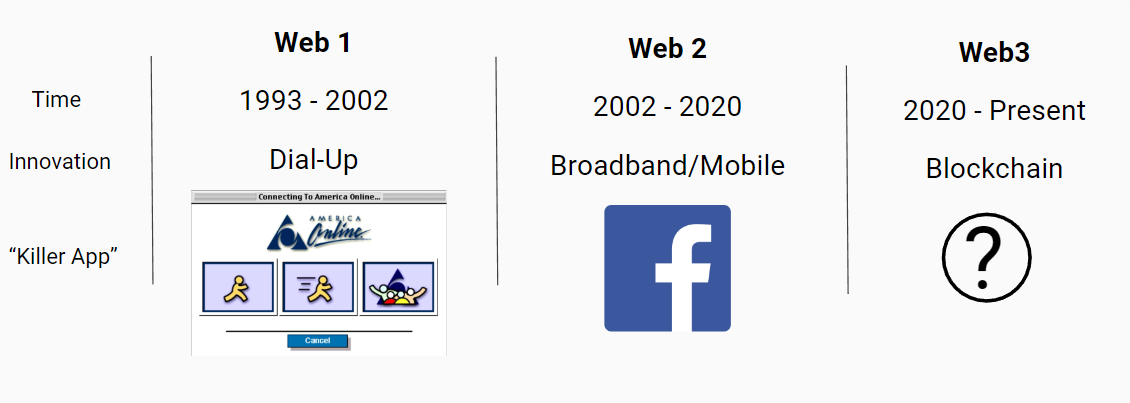

The term web3 references a new, third internet-paradigm based on blockchain technology.

- Web 1.0 (1991-2004) refers to the early internet and was characterized by dial-up and AOL.

- Web 2.0 (2004-2020) was popularized in the mid 2000s and refers to the current internet paradigm which is characterized by social media, smartphones, and cloud computing.

- Web3 (2020-Present) is the emerging internet built on top of blockchains and is characterized by increased user control, decentralization, and transparency.

While many blockchains like Bitcoin and other cryptocurrencies are focused on disrupting Wall Street and the Big Banks, builders in the web3 space are disrupting Silicon Valley and Big Tech.

Compared to large Web 2.0 platforms like YouTube and Twitter, decentralized blockchain platforms have much lower take rates. For example, Apple’s App Store requires up to 30% of all revenues from iOS app developers. In contrast, Solana’s recently launched dApp store is free of fees for users (other than network transaction fees).

Web3 has developed in response to concerns with today’s large, centralized tech platforms and their implications for user privacy, data ownership, and data security, as a decentralized alternative. Using a variety of blockchain-based technologies, web3 developers hope to make the internet more transparent and decentralized.

Web3 includes use cases such as tokenization, NFTs, decentralized identity, decentralized apps (dApps), and decentralized governance.

In the coming years, people will see increasing amounts of blockchain activity:

- T-Mobile signed a deal with blockchain-based Helium Network

- The Solana Foundation recently launched the Solana Saga smartphone

- Mercury is partnering with universities to offer NFT NIL deals to college athletes

- SpruceID is piloting blockchain-based mobile drivers licenses to give Americans more control of their data.

- GuildOne is an oil and gas royalty and land ownership platform.

More traditional software products are being disrupted by web3 alternatives:

Social Media:

Music Streaming:

Messaging:

Brief History of Blockchain

Quicker than Wikipedia

In 2008, an anonymous internet account known as Satoshi Nakamoto released a whitepaper titled Bitcoin: A Peer-to-Peer Electronic Cash System. This 9-page whitepaper laid out the author’s vision of a new, decentralized way to conduct commerce using blockchain. Bitcoin, the first blockchain, was developed in part as a response to the 2008 financial crisis and proponents argued the technology would create an alternative financial system.

Following Bitcoin’s invention, software engineers continued to experiment with new ways to use blockchains. In 2013, Vitalik Buterin, a Russian-Canadian computer programmer, released the Ethereum whitepaper, which posited a new use case for blockchains.

Buterin wanted to create a more flexible, general-purpose platform which would allow programmers to “build much more than the financial applications of the future.” Unlike Bitcoin, Ethereum is a programmable platform which developers can build and deploy applications to, enabling a new wave of innovation.

In 2015, Ethereum went live, kicking off a new wave of blockchain research and development. Ethereum allows developers to deploy “smart contracts,” which are computer programs that self-execute when certain conditions are met. Through creative software engineering, smart contracts can be used to build popular decentralized applications such as social media, e-commerce marketplaces, and video games. These decentralized applications, built on top of blockchains using smart contracts, are called dApps.

As a platform which allowed users to build new applications on top of it, Ethereum enabled new types of innovation for consumer facing products. In the same way Ethereum was an iteration on the original Bitcoin blockchain, developers have continued to iterate on Ethereum. Alternatives to Ethereum, called “Layer 1 blockchains,” have emerged, each making unique design decisions. Examples include Solana, Aptos, and Avalanche.

Other developers have focused on improving and scaling the Ethereum network called “Layer 2” blockchains because they build on top of a base, Layer 1 blockchain. Layer 2 examples include Polygon, Optimism, Arbitrum, and Starknet. Continued blockchain research and development have helped reduce costs, increase scale, and on-board new consumer applications and use cases.

-Michael

If you've made it this far, you'll probably like my other pieces as well. Subscribe below for free.